Enhancement of County own source revenue is a critical Public Financial Management reform area under Devolution. Under the Kenyan 2010 Constitution, Decentralization involves the political, administrative and fiscal autonomy of the 47 Counties from the National Government.

While many scholars and pundits may debate or even question the practicality of this philosophy, the acceptable school of thought is counties need to be able to sustainably generate more of their own revenues to finance their development and operational needs, without entirely relying on the National Exchequer.

2010 Constitutional foundation of Own Source Revenue

To better understand why own source revenue mobilization remains a n important area of PFM Focus, let us begin by understanding the basis of this from the 2010 Constitution. Own Source Revenue (OSR) is governed by national legislations; 2010 Constitution, the 2012 Public Finance Management Act, the County Government Act of 2012 and the 2011 Urban Areas and Cities Act 2011.

The Constitution defines County Governments’ funding sources to include:

a) Equitable share of at least 15 percent of most-recently audited revenue raised nationally (Article 202(1) and 203(2));

b) Additional conditional and unconditional grants from the National Government’s share of revenue (Article 202(2));

c) Equalization Fund based on half of one percent of revenue raised nationally (Article 204);

d) Local revenues in form of taxes, charges and fees; and,

e) Loans and grants.

The 2020 Constitution allows Counties to impose:

a) Property rates;

b) Entertainment taxes;

c) Charges for services they provide; and,

d) Any other tax or licensing fee authorized by an Act of Parliament.

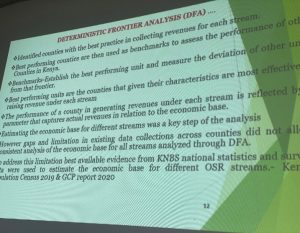

From the above, one can be able to understand the specifics revenue streams available for counties to generate revenues. In recent times, a number of studies have been carried out to determine optimal revenues that the 47 counties can collect.

One of this report, which informed this blog, is the Comprehensive Own Source Revenue (OSR) Potential and Tax Gap Study developed by the Commission on revenue Allocation. The assessment determined the maximum possible own source revenue that each county government can collect from the most important revenue streams when they apply the best practices in revenue administration.

PFM Reforms 2018-2023 CRA Activity work-plan

As part of implementing its activities , as outlined in the PFM Reforms strategy 2018-2023 , The PFMR Secretariat supported the commission on Revenue allocation to conduct a cost of Own Source Revenue Study targeting 5 pilot counties namely Laikipia , Embu Kakamega , Marsabit and Kwale.

The primary focus was to gather data on the costs associated with Own Source Revenue (OSR) collection within the County.

This article will however restrict its focus to the validation study conducted on Kwale County Government. A team of officers from the Commission on Revenue Allocation and PFM Reforms Secretariat, led by the CRA Director of Fiscal, CPA Roble Said Nuno led an assessment of Kwale County Revenue Administration and Enforcement Framework. Interviews and discussions were held with the County senior revenue officials, collectors, and enforcement officers in various locations within and outside Kwale County.

Meetings with officers from Kwale County Government

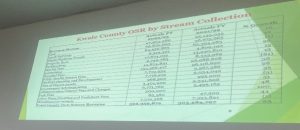

The first engagement involved an introduction meeting with the Kwale County Government team led by the Director of Revenue CPA Samira Swaleh. The two teams had a chance to go through a presentation done by CRA, detailing the information and data on Kwale County, its Revenue targets, and identify gaps between maximum potential revenues and actual collections.

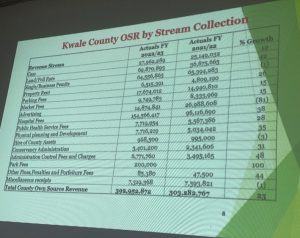

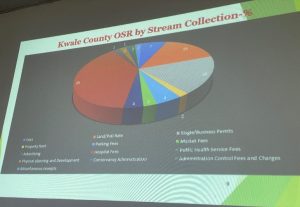

Key Highlights from the report.

From the presentations done by CRA, it is estimated that Kwale County has the potential to collect 3.2Billion shillings from the current.

Notable issues brought forward by officers from Kwale County Government.

During the discussions, the team from Kwale County Government raised concerns over the actual Data utilized as reference points in the Commission on Revenue Comprehensive Own Source Revenue (OSR) Potential and Tax Gap Study, pointing to a lack of validation by both parties. To remedy this, the commission, through the Director of Fiscal affairs, agreed to convene a follow up meeting aimed at ironing out the emerging issues.

The officers later conducted a number of field visits at revenue collection points in the county aimed at familiarizing themselves with the ‘actual’ situation ‘kwa ground’ as well as ascertaining the actual Data. A number of areas we visited included the Shimoni and Lunga Lunga Border points, the team visited a number of markets such as Kombani,Matuga,Lunga lunga and Kinango markets.

Identified Gaps from the field visit

1. Lack of proper accountability of daily cash collected. A number of revenue collection sites employed cash collection with manual receipt production.

2. Lack of minimum required tools at the revenue collection and enforcement work place by officers.

3. Lack of minimum basic amenities at revenue collection point such as work shelters for officers.

4. Lack of transport for staff manning the Cess collection points.

About the Cost of OSR collection Study

The CRA study is driven by the need to solve one of the pressing challenges in revenue administration and management, identified in the National Policy to Support Enhancement of County Own Source Revenue – weak understanding of county revenue administration costs. The cost of revenue administration at the county level is not well understood and research data is lacking.

CRA opted to conduct the Cost of OSR Collection study in five pilot counties, three of which have Revenue Boards and two have revenue departments. After concluding the data collection, the data will be analyzed then presented in a report, to be validated by County Revenue Boards and Directors of Revenue in the piloted counties.

")

")